Financial planning for medical professionals: Smart money strategies

financial planning for medical professionals: Learn debt management, investing, and tax tips for a sustainable, burnout-free career.

Financial planning isn't just for Wall Street types. For those of us in medicine, it’s a critical tool for survival—a way to translate a demanding, high-stakes career into genuine wealth, career autonomy, and personal well-being.

Why Your Medical Career Demands a Unique Financial Plan

After years of grueling training, finally earning a physician, NP, or PA salary feels like crossing the finish line. But that high income is just one vital sign of your financial health, not the complete picture.

The reality for most clinicians is a financial life defined by two extremes: a significant income paired with staggering student loan debt, which often blows past $200,000. This dynamic creates a unique set of challenges that generic, cookie-cutter financial advice simply doesn't cover.

Without a plan tailored to your career, that six-figure salary can vanish. It gets eaten away by massive debt payments, high taxes, and the quiet, insidious creep of "lifestyle inflation." On top of that, the intense demands of medicine mean time is your most scarce resource, making the idea of managing your finances feel completely overwhelming.

Your Finances as a Patient Chart

Think of your financial life like a patient's chart. A high income is like a strong heartbeat—it’s crucial, but it doesn't tell you anything about the patient's overall wellness. A real financial plan is your personalized treatment protocol. It starts with a thorough diagnosis of your current state, sets a clear strategy for the future, and requires consistent follow-ups to stay on track.

This guide provides that framework. We're moving beyond generic advice to give you a clinician-specific roadmap that covers the core pillars of your financial health.

A well-structured financial plan is the key to transforming your hard-earned income into lasting financial freedom. It gives you the control to sidestep burnout, make career moves based on passion instead of necessity, and build a life that actually reflects your values.

Before we dive deep into strategies for student loans, investing, and contract negotiation, let's get a high-level view of the territory we'll be covering. The table below outlines the essential components of a healthy financial life for any medical professional.

The Medical Professional's Financial Health Checklist

| Financial Pillar | Key Objective | First Action Step |

|---|---|---|

| Debt Management | Systematically eliminate high-interest debt, especially student loans, to free up cash flow. | Choose the right repayment plan (e.g., PAYE, REPAYE, or private refinancing) for your goals. |

| Asset Protection | Shield your income and assets from career-ending disability, lawsuits, or unforeseen events. | Secure a specialty-specific disability insurance policy before you need it. |

| Wealth Accumulation | Grow your net worth through tax-efficient retirement accounts and strategic investing. | Open and max out a Roth IRA or Backdoor Roth IRA. |

| Career Optimization | Align your job choices with your financial goals for a sustainable, fulfilling career path. | Negotiate your next contract with a clear understanding of your market value and lifestyle priorities. |

Mastering your finances isn't just about growing a portfolio; it's about securing your future. It's the critical step that ensures your years of dedication to medicine translate into a life of security, choice, and peace of mind.

This guide will show you exactly how to take back control, one step at a time.

Building Your Financial Foundation by Conquering Debt

Most clinicians walk away from graduation with a diploma in one hand and a student loan balance of over $200,000 in the other. Navigating repayment feels a lot like clinical practice—picking the wrong plan is like prescribing the wrong treatment, and the side effects can be brutal.

Think of your loan strategy like a treatment plan for your financial health. You wouldn't give every patient the same drug, and you shouldn't treat all student debt the same way.

Income-driven options like PSLF, PAYE, and REPAYE are your targeted therapies, each designed for a specific financial "condition." The key is matching the right plan to your unique situation—your income, family size, and career goals.

- PSLF: This is for clinicians in eligible public service or non-profit roles. It offers loan forgiveness after 120 qualifying payments, but you have to stay on top of the annual paperwork to ensure you remain on track.

- PAYE: This plan caps your payments at 10% of your discretionary income and forgives the remaining balance after 20 years of payments. It's often a good fit for those with high debt-to-income ratios early in their careers.

- REPAYE (now SAVE): This plan also ties payments to income but extends the forgiveness timeline to 25 years for graduate loans. A key feature is its interest subsidy, which can prevent your loan balance from ballooning.

- Private Refinancing: This is like switching to a different medication entirely. It can significantly lower your interest rate, but you lose all federal protections and access to forgiveness programs. It's a permanent decision.

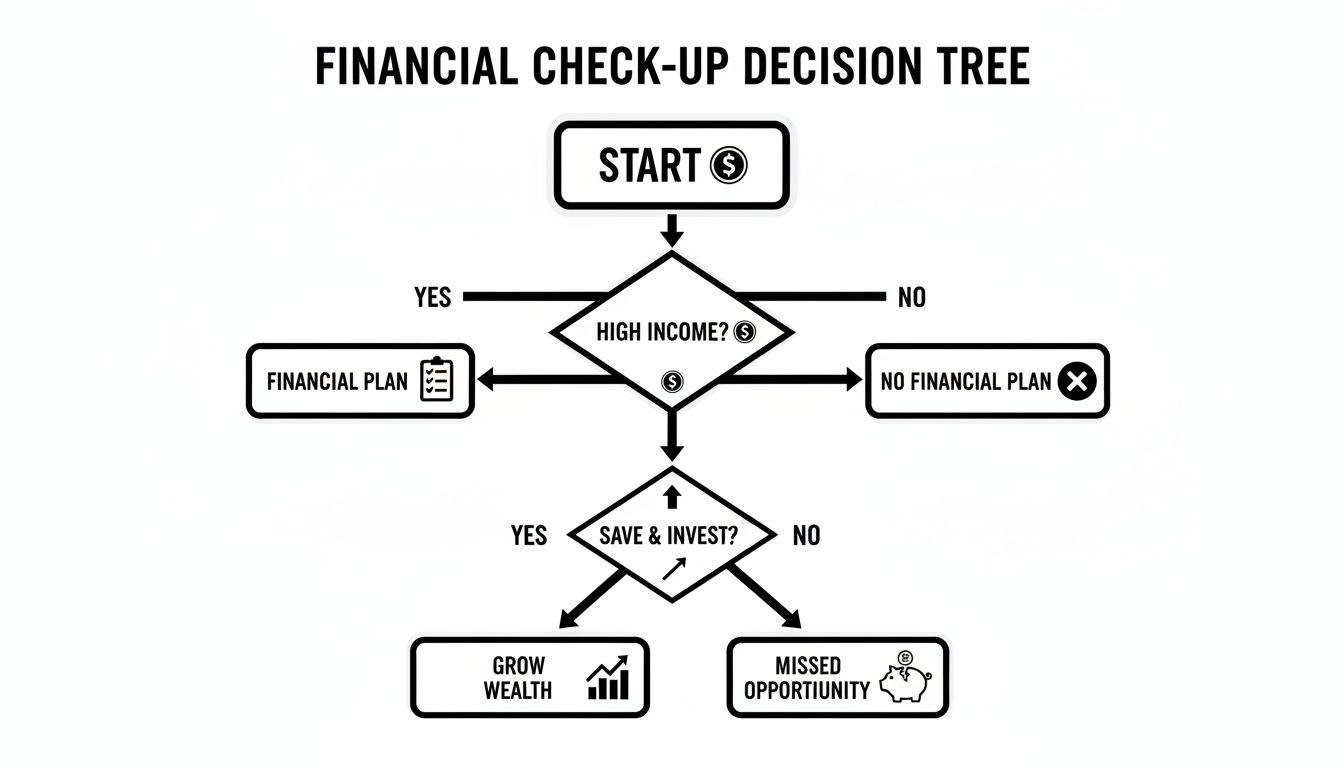

This decision tree gives you a quick visual check-up. Are you on a path to financial health, or are there missed steps creating risk?

As you can see, simply having a plan is the first step toward avoiding nasty surprises down the road.

Creating a Clinician-Specific Budget

Once your debt plan is in place, it's time to build a budget that reflects the realities of a clinician's income. Your pay isn't always a simple, predictable salary; it often includes variable income from locums work, bonuses, and on-call stipends.

A standard budget template just won't cut it. You need to account for the unique costs of our profession.

- Track all income streams separately. Don't let locums pay just blend into your main account.

- Budget for professional expenses first. Earmark money for licensing fees, board certifications, and CME before you calculate your personal spending.

- Don't forget professional dues. Memberships to associations are a real cost that needs a line item.

Dr. Patel, a hospitalist who picks up locums shifts, puts 20% of her extra earnings into a separate "career costs" bucket. This simple move means her biannual licensing fees never force her to pull from her personal savings. It's a small system that dramatically reduces financial stress.

Building Your Emergency Fund

Think of an emergency fund as your personal malpractice insurance against life. It’s the financial cushion that protects you when the unexpected happens—a job loss, a medical issue, or a family crisis.

Without it, you’re one bad event away from derailing your entire financial plan.

- Aim for 3–6 months of essential living expenses. Keep this in a liquid, high-yield savings account, not tied up in investments.

- Automate it. Set up a recurring transfer from your checking to your emergency savings each payday.

- Re-evaluate annually. If you get a big raise, have a child, or buy a home, your fund size needs to adjust.

A healthy emergency fund gives you freedom. It’s the difference between making career choices based on passion versus making them out of panic.

This financial stability is crucial when evaluating new opportunities. You can see how different job offers might impact your overall financial picture with WeekdayDoc's Offer Analyzer.

Leveraging Forgiveness and Refinancing

With such a significant debt load, understanding the specific student loan forgiveness programs available to medical professionals is non-negotiable. This is where you can save tens, or even hundreds, of thousands of dollars.

The two main paths—forgiveness and refinancing—are mutually exclusive for any given loan, so the choice is a major one.

- Forgiveness: Programs like PSLF or income-driven plans can erase your debt years ahead of schedule, but they come with strict requirements.

- Refinancing: This can slash your interest rate, potentially as low as 3%, but you give up federal benefits like forbearance and forgiveness eligibility forever.

- Hybrid Strategy: You can have the best of both worlds. Keep your federal loans on a forgiveness track while privately refinancing any high-interest private loans you might have.

Take Dr. Nguyen, a radiologist. During her fellowship, her income was low, so she used the REPAYE plan to keep payments manageable and benefit from the interest subsidy. Once she became an attending and her salary jumped over $250,000, she refinanced her federal loans to lock in a much lower interest rate, saving a fortune over the life of the loan.

The right choice depends entirely on your career path, your specialty's income potential, and your tolerance for risk. Tackling your debt with a clear strategy doesn't just clear a number from a balance sheet; it gives you the freedom to focus on your patients and build a life you actually enjoy.

Protecting Your Most Valuable Asset: Your Ability to Earn

Once you have a handle on your student loans, the game shifts from offense (accumulation) to defense (protection). It’s tempting to focus only on building up your savings and investments, but your single most valuable asset isn’t what’s in your bank account today.

It's your ability to earn a high income for the next 20 to 30 years.

This future earning potential is literally worth millions. Protecting it isn’t just a good idea—it’s an absolute necessity for anyone in a demanding medical career. Insurance is how you build that shield.

Disability Insurance: The Non-Negotiable Shield

Think about it: if an injury or illness keeps you from working, your income disappears overnight. But your mortgage, student loan payments, and other bills don't. This is where disability insurance steps in, forming the bedrock of your financial defense. It replaces a big chunk of your income, usually 60-70%, so you can keep your life on track without draining your savings.

But not all policies are the same. For doctors, one feature is an absolute deal-breaker: "own-occupation" coverage. This is the critical detail that separates a truly protective policy from one that could let you down.

An "own-occupation" policy defines disability as being unable to do the specific duties of your medical specialty. This is worlds apart from an "any-occupation" policy, which only pays out if you can’t work in any job at all.

Let’s play that out. A surgeon develops a hand tremor and can no longer operate.

- With an "own-occupation" policy: She’s considered disabled because she can no longer be a surgeon. She gets her full benefit, even if she decides to pivot to teaching or consulting.

- With an "any-occupation" policy: The insurance company could argue that since she can still teach or do administrative work, she isn’t truly disabled. Her claim could be denied.

For a clinician, that difference is everything. It protects the highly specialized career you spent more than a decade building. Locking in a solid own-occupation policy during residency or fellowship is one of the smartest financial moves you'll ever make.

Malpractice Insurance: Claims-Made vs. Occurrence

Malpractice insurance is a cost of doing business in medicine, but you need to know what kind of policy you have. This becomes especially important when you change jobs, as getting it wrong can leave you with a massive, unexpected bill.

The two main flavors are:

- Occurrence Policies: These cover any incident that happened while the policy was active, no matter when the lawsuit is actually filed. It’s the simpler, more comprehensive option, but it usually costs more upfront.

- Claims-Made Policies: These only cover claims that are filed while the policy is active. If you leave that job, you’re exposed. You’ll need to buy separate "tail coverage" to protect yourself from any incidents that occurred during your employment. Tail can be brutally expensive, sometimes costing 200% of your last annual premium.

When you're negotiating a contract, always ask who pays for tail coverage if you leave. Getting that one point clarified can save you tens of thousands of dollars down the road.

Life and Umbrella Insurance: Completing Your Armor

While disability insurance protects your income stream, a couple of other policies are essential for protecting your family and your net worth.

- Life Insurance: The main point of life insurance is to replace your income for your dependents if you die unexpectedly. For most doctors, term life insurance is the way to go. It’s simple and cost-effective, providing a large payout for a set period (like 20 or 30 years) while your kids are young and you still have a mortgage. Whole life policies are often sold as an investment, but they are far more expensive and rarely the best tool for the job.

- Umbrella Policies: This is extra liability coverage that kicks in after your auto or homeowners insurance limits are maxed out. As a physician with a high income and visible assets, you're a potential target for lawsuits. A personal umbrella policy for $1 million or more is a cheap way to protect everything you’ve worked for from a worst-case scenario.

Getting your insurance strategy right is the defensive side of your financial plan. It ensures that one bad break—an illness, an accident, or a lawsuit—doesn’t completely derail a lifetime of hard work.

Supercharge Your Savings with Retirement and Tax Strategies

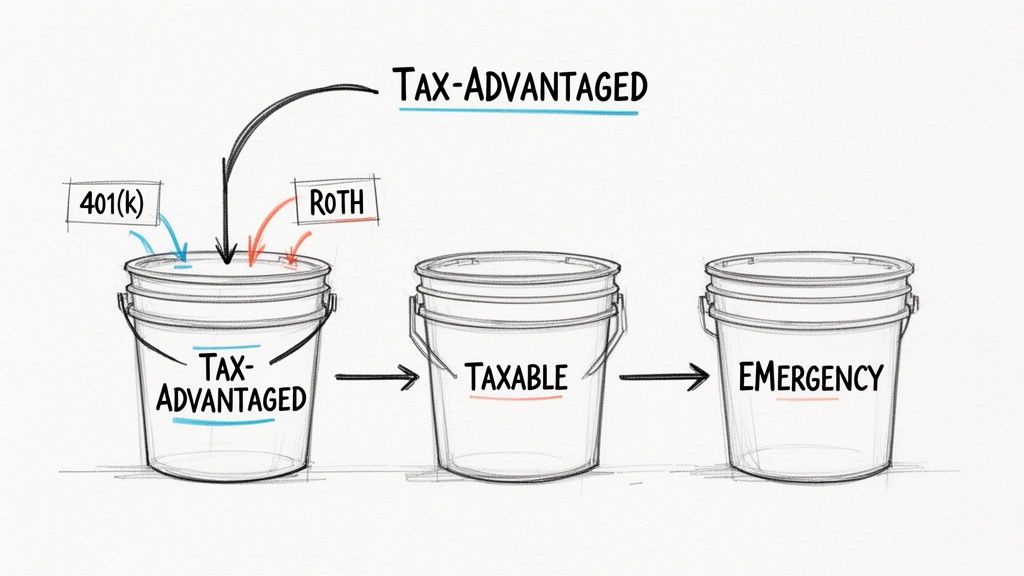

Once you’ve built your defensive line with the right insurance, it's time to go on offense. This is where you put your money to work, actively growing your wealth and speeding up the journey to financial freedom. And the most powerful tools in your playbook? Tax-advantaged retirement accounts. Think of them as savings superchargers.

I find it helps to picture your savings strategy as filling different buckets, each with its own special purpose. The trick is to fill them in the right order. Do it correctly, and you’ll capture the most "free money" from things like employer matches and get the biggest possible tax breaks from the government. This methodical approach is how you turn a high income into real, lasting wealth.

Decoding the Retirement Account Alphabet Soup

The world of retirement plans is notoriously full of confusing acronyms. For clinicians, the most common options you'll see are 401(k)s and 403(b)s, which are typically offered by employers. They're pretty similar in how they work, but the real key is knowing how to use them to your advantage.

Your absolute first priority should always be contributing enough to get your full employer match. This is an instant, guaranteed return on your money—often 50% or even 100%. Not taking the match is literally like turning down a bonus with every single paycheck. It’s the lowest-hanging fruit in finance.

The Bucket Analogy for Prioritizing Savings:

- Bucket 1 (The Match): Put just enough into your 401(k) or 403(b) to get the full employer match. No more, no less for now.

- Bucket 2 (The Roth): Next, max out a Roth IRA. If your income is too high, execute a Backdoor Roth IRA. This bucket gives you tax-free growth and, crucially, tax-free withdrawals in retirement.

- Bucket 3 (The Max-Out): Now, circle back to your 401(k)/403(b) and contribute until you hit the annual IRS limit.

This sequence ensures you grab the free money first, then lock in tax-free growth, and finally, maximize your tax-deferred savings. For a deeper look at different investment strategies, we have more guides at https://www.weekdaydoc.com/guides.

Unlocking Advanced Strategies

Once you're consistently maxing out your main retirement accounts, you can start exploring more advanced techniques to really optimize your finances. They might sound complicated, but the core ideas are actually quite straightforward.

For instance, the Health Savings Account (HSA) is one of the most powerful tools out there. It has a unique triple-tax advantage: your contributions are tax-deductible, the money grows tax-free, and any withdrawals for qualified medical expenses are also tax-free. Many savvy clinicians use it as a stealth retirement account specifically for healthcare costs down the road.

Another powerful move is tax-loss harvesting. This involves selling an investment in your taxable brokerage account that has gone down in value. You then use that loss to offset capital gains taxes from your winning investments, which lowers your overall tax bill without really changing your portfolio's long-term plan.

How Your Job Status Changes Everything

Whether you’re a W-2 employee or a 1099 independent contractor has a massive impact on your retirement and tax planning options. This choice isn't just about your day-to-day work; it can either limit your financial tools or unlock some incredibly powerful ones.

- W-2 Employees: You generally get access to an employer-sponsored plan like a 401(k). It’s convenient, for sure, but you're stuck with whatever investment options and contribution rules that specific plan offers.

- 1099 Contractors: As a contractor, you're considered self-employed. This opens the door to a Solo 401(k). This account is a game-changer because it lets you contribute as both the "employee" and the "employer," allowing you to save significantly more than a traditional 401(k)—often over $60,000 per year.

Choosing a locums or other 1099 role can be a deliberate strategic move to take more control over your financial future. The ability to open a Solo 401(k) gives you a much higher savings ceiling and total freedom over your investment choices, which can dramatically speed up your path to financial independence.

Investing Beyond Your Retirement Accounts

So, you’ve maxed out your retirement accounts. Congratulations—that’s a huge milestone. The natural question is, what’s next?

The answer for most clinicians is a taxable brokerage account. This is your engine for building serious long-term wealth and, just as importantly, financial flexibility long before you hit traditional retirement age.

Think of a diversified brokerage account like a well-balanced diet for your portfolio. It’s what fuels steady, healthy growth while protecting you from the inevitable ups and downs of the market. You wouldn't eat only one food group, and you shouldn't invest in only one type of asset. Mixing stocks, bonds, and alternatives is just like combining fruits, proteins, and grains to keep your body running strong.

This is especially critical for physicians. Healthcare costs are projected to skyrocket, and a PwC report warns that these trends could eat up a huge chunk of your income if you're not prepared. Proactive planning, which includes investing beyond your 401(k), is your best defense.

Build a Well-Balanced Portfolio

Your portfolio’s “diet” should be a solid mix of different asset groups. A common starting point looks something like this:

- Equities (Stocks): These are your growth engine. It's smart to balance large-cap stocks (big, stable companies) with small-cap ones to get exposure across the entire market.

- Bonds: Think of these as your portfolio’s stabilizer. A mix of government and corporate bonds can help smooth out the ride when the stock market gets choppy.

- Real Estate: This adds another layer of diversification and potential income, whether you own property directly or through REITs (Real Estate Investment Trusts).

- Health Tech: You have a unique, insider’s perspective on the industry. Why not put it to use?

A diversified portfolio is your best defense against unexpected market “sickness” and ensures healthier returns over time.

Asset Allocation Strategies

Deciding on your mix really comes down to your personal risk tolerance. How much volatility can you stomach? Here’s a simple framework to get started:

- Define your timeline and goals. Are you saving for a house in five years or for financial independence in twenty? Your timeline dictates how much risk you can afford to take.

- Set target percentages for each asset class. A common rule of thumb is the "110 minus your age" rule for stock allocation, but you can adjust this based on your own comfort level.

- Rebalance once a year. Life happens, markets move, and your portfolio will drift. Annually nudging it back to your target percentages keeps you on track and disciplined.

This process is what prevents you from making emotional decisions, like panic-selling during a downturn or chasing a hot stock.

Real Estate Vehicles

For clinicians looking to add real estate to their portfolio, there are two main roads you can take: direct ownership or REITs.

| Feature | Direct Ownership | REITs |

|---|---|---|

| Minimum Investment | Often $100,000+ | As low as $500 |

| Liquidity | Low – tied up in property | High – trades like a stock |

| Management | Hands-on maintenance required | Professionally managed portfolios |

| Tax Benefits | Depreciation and interest | Dividend income and 1031 options |

Direct ownership gives you ultimate control but comes with the headaches of being a landlord. REITs, on the other hand, offer passive exposure to real estate with a much lower barrier to entry.

Investing in Health Tech

As a clinician, you see what’s working—and what isn’t—on the front lines of medicine every day. That’s a powerful edge. You could consider investing in areas like:

- Biotech startups tackling unmet clinical needs.

- Telehealth platforms that are actually improving patient access.

- Medical device companies with innovative products you believe in.

These can be higher-risk, higher-reward plays. Just be sure to balance them with the boring-but-effective foundation of your portfolio, like low-cost index funds.

Tax Efficiency and Harvesting

Taxes are one of the biggest drags on investment returns in a brokerage account. The key is to be smart about it.

Any investment you hold for over one year qualifies for lower long-term capital gains rates. Sell before that one-year mark, and you’ll pay taxes at your ordinary (and much higher) income tax rate.

Another powerful strategy is tax-loss harvesting. When the market takes a dip, you can sell a position that’s at a loss. This allows you to:

- "Harvest" that loss to offset taxable gains elsewhere in your portfolio.

- Free up that cash to reinvest in a similar (but not identical) asset, so you don't miss the eventual rebound.

- Over decades, this can significantly boost your after-tax returns.

Using WeekdayDoc Tools

Wondering how a more aggressive brokerage strategy might speed up your path to financial independence?

Plug your numbers into WeekdayDoc’s Salary & FIRE Calculator. You can model different scenarios by adjusting your expected investment returns and savings rate to see exactly how it impacts your FIRE timeline.

You can also use your Burnout Index score to find a work-life balance that gives you the mental and financial capacity to save more. Combining these tools helps you make an informed decision on how hard to press the accelerator with your investments.

Example Clinician Portfolio

Dr. Lee, a hospitalist in her late 30s, allocates her taxable account with 60% stocks, 30% bonds, and 10% in REITs. Every January, she rebalances her portfolio to get back to that target mix. This strategy aims for solid growth while keeping volatility in check.

The key is to have a plan and stick with it. Review your portfolio's performance, but don't obsess over it. Set up automated tools to make rebalancing and tax-loss harvesting simple, and let your money do the work for you.

How Your Career Choices Shape Your Financial Future

Your career isn’t just a string of clinical decisions—it's a series of major financial ones. Every choice you make, from the type of practice you join to the call schedule you accept, has a direct ripple effect on your net worth, your timeline to financial independence, and maybe most importantly, your own well-being. Thinking about your finances without connecting them to your career is a huge missed opportunity.

When a job offer lands in your inbox, it's tempting to fixate on the salary. But that big number can easily hide hidden costs—to your time, your energy, and your long-term financial health. The real value is buried in the total compensation package.

You have to look at the benefits that actually build wealth and give you a safety net:

- Retirement Match: An employer match is literally a 100% return on your money, right out of the gate. A job with a lower salary but a killer match can easily put you ahead of a higher-paying one with nothing.

- Insurance Benefits: Good disability and health insurance through an employer can save you thousands of dollars a year compared to buying policies on your own.

- Partnership Tracks: A clear path to partnership means equity and a share in the profits. That’s a powerful wealth-building engine that a simple salaried job just can't offer.

The True Cost of a Demanding Job

Let's break it down with a realistic comparison for a physician assistant.

Offer A: The Grinder

- Salary: $150,000

- Schedule: A beast. Frequent on-call nights and weekends.

- Retirement: 3% 401(k) match.

Offer B: The Balancer

- Salary: $135,000

- Schedule: Weekdays only. No call, no weekends.

- Retirement: 6% 401(k) match.

On the surface, Offer A looks like the clear winner with its $15,000 salary bump. But that intense schedule comes with a steep, often hidden, price. We know burnout and compensation pressures are squeezing clinicians hard, making work-life balance a non-negotiable for building sustainable wealth. As medical groups face financial pressure, it's often the clinicians who pay the price with brutal schedules, which is why finding a balanced role is a massive advantage. The AMGA has some great survey data on these industry-wide challenges at amga.org.

Time Wealth: The Ultimate Multiplier

The secret weapon in Offer B is the "time wealth" it creates. Having your nights and weekends back gives you a huge surplus of personal time and mental energy—assets you can reinvest for incredible returns.

Time wealth is the freedom to use your non-working hours to build a richer life, whether that means launching a side hustle, spending priceless time with family, or simply recovering from the demands of patient care. This is the resource that accelerates sustainable financial independence.

So, what can you do with all that reclaimed time?

- Generate Extra Income: You could start a telehealth side gig, do some medical writing, or take on consulting work. An extra $1,000-$2,000 a month from a side hustle can completely wipe out that initial salary difference.

- Slash Your Expenses: More time at home means you're more likely to cook instead of ordering expensive takeout after a long shift. That alone can save you thousands every year.

- Invest in Your Well-being: Getting proper rest and exercise is your best defense against burnout, which is a massive financial risk. A burned-out clinician is less productive and far more likely to make a costly, reactive career change.

The WeekdayDoc Salary & FIRE Calculator makes it crystal clear how these seemingly small adjustments can completely change your financial trajectory.

This screenshot shows it perfectly: a slightly lower salary combined with a higher savings rate—made possible by a better work-life balance—can get you to financial independence years earlier.

At the end of the day, the balanced career choice often creates a faster and, more importantly, a more sustainable path to your financial goals. You can plug in your own numbers with our Salary & FIRE Calculator Pro to see the real-world impact for yourself.

Physician Finance FAQs

Let's tackle some of the most common money questions that come up for doctors. These are the practical, real-world decisions you'll face at different stages of your career.

Should I Pay Off Student Loans Aggressively or Invest?

This is the classic debate, and honestly, the answer comes down to math and your personal risk tolerance. The simple answer is to look at the interest rates.

If your student loans have a low interest rate (think under 5%), you'll likely come out ahead by investing. The historical returns of the stock market usually beat that number over the long haul. But if you're staring down high-interest private loans, paying those off is like getting a guaranteed, tax-free return on your money—you can't beat that.

For most people, a hybrid approach feels right:

- First, always contribute enough to your 401(k) or 403(b) to get the full employer match. It's free money. Don't leave it on the table.

- Next, throw any extra cash you have at high-interest debt (anything over 6-7%). Get rid of it as fast as you can.

- Once that expensive debt is gone, you can pivot and funnel that extra money into your investments.

How Much Disability Insurance Do I Really Need?

You want a policy that covers 60-70% of your gross income. It sounds like a lot, but if you pay the premiums yourself with after-tax money, the benefit comes to you tax-free. That means the policy should replace nearly all of your current take-home pay.

The single most important part of any policy is the "own-occupation" definition of disability. This is non-negotiable. It means you get paid if you can no longer do the specific duties of your medical specialty, even if you could technically go work another job.

When Should a Clinician Hire a Financial Advisor?

There's no magic moment, but it's usually time to get professional help when your financial life starts feeling complicated. Big life events are often the trigger: finishing residency, buying a house, starting a family, or realizing your investment portfolio has grown to a size that makes you nervous.

When you do look for an advisor, make sure they are a fee-only fiduciary. A fiduciary is legally required to act in your best interest—not a salesperson pushing a product. Look for the CFP® designation and ask them directly about their experience working with physicians. Our financial lives just have different challenges and opportunities.

Ready to align your career with your financial goals? At WeekdayDoc, we curate burnout-friendly jobs that give you back your time, so you can build the life you want. Find your next no-call, no-weekend opportunity.